A Tale of Two Decades: Lessons for long-term investors

A year like 2022 can test even the most committed long-term investor. With the benefit of 20/20 hindsight, we can all say we saw the market drop coming or that interest rates were obviously going to dramatically increase. Unfortunately, when you’re in the moment, clarity is always difficult. When markets are going up, there’s the desire to stay on the ride because you don’t want to risk missing out on future gains. In the end, as we’ve written so many times over the years, trying to time markets is nearly impossible.

Dimensional offers a look back at the first two decades of the 21st century (2000 – 2009; 2010 – 2019) to provide us with lessons in both timing and diversification1. For long-term investors, it’s information worth repeating. For those investors who think too short-term, they may be lessons worth learning.

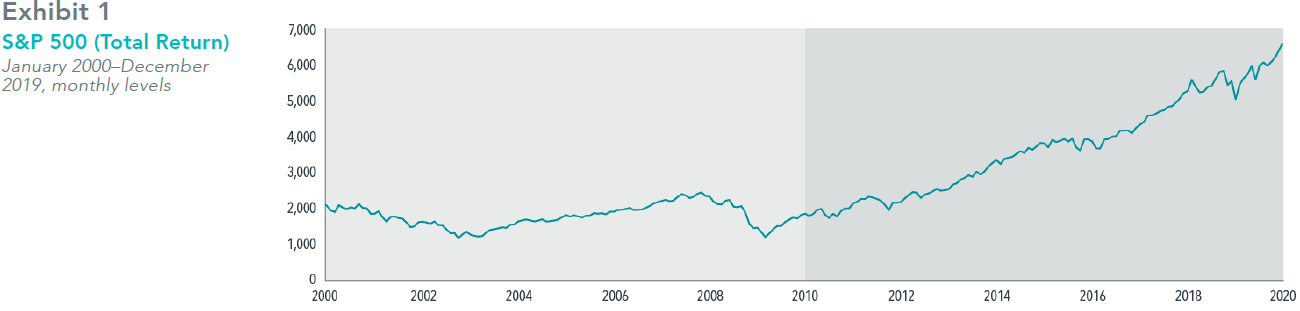

A chart showing the performance of the S&P 500 from 2000-2019 is impressive, especially when viewing only the start and end dates (see Ex. 1). As with all things financial, the devil is in the details.

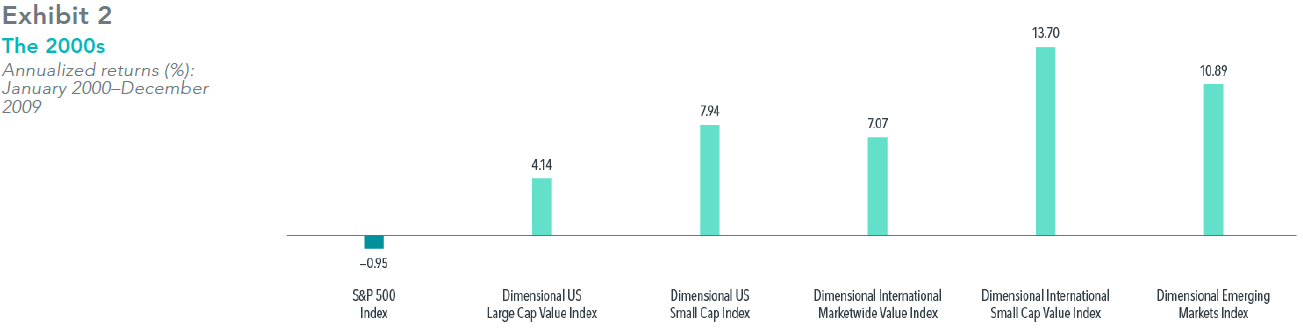

The Lost Decade: The period 2000 – 2009 is often referred to as The Lost Decade. Prior to the year 2000, the S&P 500, which is primarily viewed as a domestic large cap stock index, had averaged more than 10% in annualized gains. During The Lost Decade, however, the S&P 500 averaged annual losses of 0.95% (See Ex. 2). “Yet it was a good decade for investors who diversified their holdings globally beyond U.S. large cap stocks and included other parts of the market with higher expected returns – companies with small market capitalizations or low relative price (value stocks).” In fact, for the entire decade, asset classes such as U.S. large cap value, U.S. small cap, international large cap value, international small cap value, and emerging markets all had annualized gains that dwarfed the S&P 500.

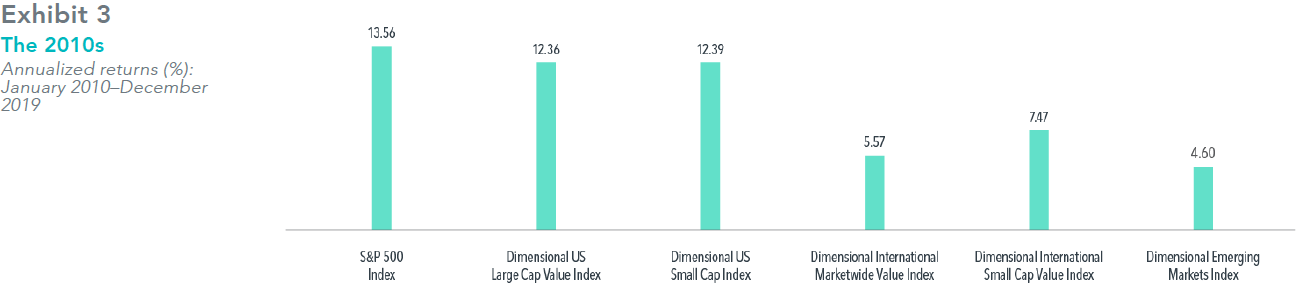

Flipping the Script: “The next period…reveals quite a different story.” In fact, the star performer for the decade 2010 - 2019 was the S&P 500, with average annualized gains of 13.56%. (U.S. large cap value and U.S. small cap weren’t too far behind.) International and emerging markets had positive returns but were no longer in the forefront. (See Exhibit 3) This was nearly the complete opposite of the previous decade.

Lessons Reaffirmed: A Tale of Two Decades is noteworthy because it reinforces not only the need to own a diversified portfolio but the necessity to periodically and opportunistically rebalance it. When the performance of one asset class within the portfolio greatly exceeds the performance of another asset class, it’s important to sell a slice of the out-performer and invest those dollars into one of the portfolio’s laggards. At some point, whether it’s months, years, or even an entire decade, we’ve seen that out-performing asset classes eventually slow and give way to other parts of the market. Similarly, under-performers will, at some point, exceed expectations. While we may not know when these events will occur, we’ve seen that they do. Rebalancing allows a portfolio to take advantage of growth opportunities and minimize losses, losses that might have been even more pronounced if an investment category had been allowed to grow too large2.

1 “A Tale of Two Decades: Lessons for Long-Term Investors.” Dimensional, 28 Dec. 2022.

2 Kinniry, Francis M., et al. “Putting a Value on Your Value: Quantifying Advisor's Alpha.” Vanguard, July 2022.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by S.F. Ehrlich Associates, Inc. (“SFEA”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from SFEA. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. SFEA is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SFEA’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a SFEA client, please remember to contact SFEA, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, or revising our previous recommendations and/or services.