If You're 46 And Unhappy, There May Be Good News...

If You're 46 And Unhappy, There May Be Good News...

S.F. Ehrlich Associates |

March 31, 2019

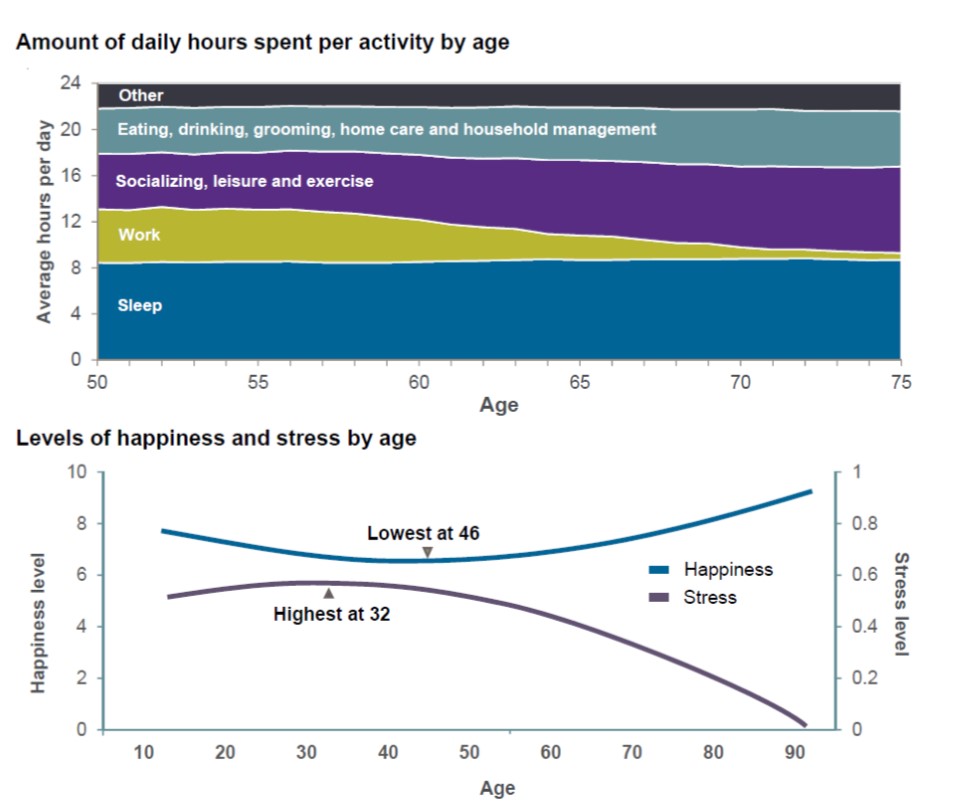

JP Morgan’s 2019 Guide to Retirement includes a chart (see below) depicting levels of happiness and stress by age. For married Americans, happiness is lowest at age 46 and then continues to rise on an upward sloping curve all through the ‘golden’ years. (I wonder if it has anything to do with the kids’ finally going off to college.)

In contrast, stress levels are highest at age 32, which is probably the age that parents kick their children out of their basement to move into their own apartment. In general, stress levels drop thereafter.

The two determinants that appear to cause less stress and more happiness: an increase in time spent each day on the category “Socializing, leisure, and exercise,” and a decrease in time spent each day “Working.”

Roy, Katherine, et al. “J.P. Morgan Guide to Retirement, 2019 Ed.”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by S.F. Ehrlich Associates, Inc. (“SFEA”), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from SFEA. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. SFEA is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SFEA’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a SFEA client, please remember to contact SFEA, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing, evaluating, or revising our previous recommendations and/or services.