Stan's World - Control Issues

It would only be a slight exaggeration to say I prefer getting to airports long before my flight is scheduled to depart. I want to have an unhurried drive, a calm wait as I go through security, buy some snacks, sit down, and put my feet up. At least for this part of the journey, I want to be in control.

Ideally, I would prefer to even fly the plane, though that’s unlikely to ever happen. First, I’m above the maximum age for commercial pilots, which is really just a minor point. Second, I’m not a licensed pilot. (I’ll admit that’s a more significant point.) Third, I don’t like heights. Fourth, my control issues would dictate that I would shut the doors and push back from the gates whenever I was ready to go, neglecting such critical details as scheduled departure times and whether (or not) the passengers were even seated. Or the tanks were filled with gas.

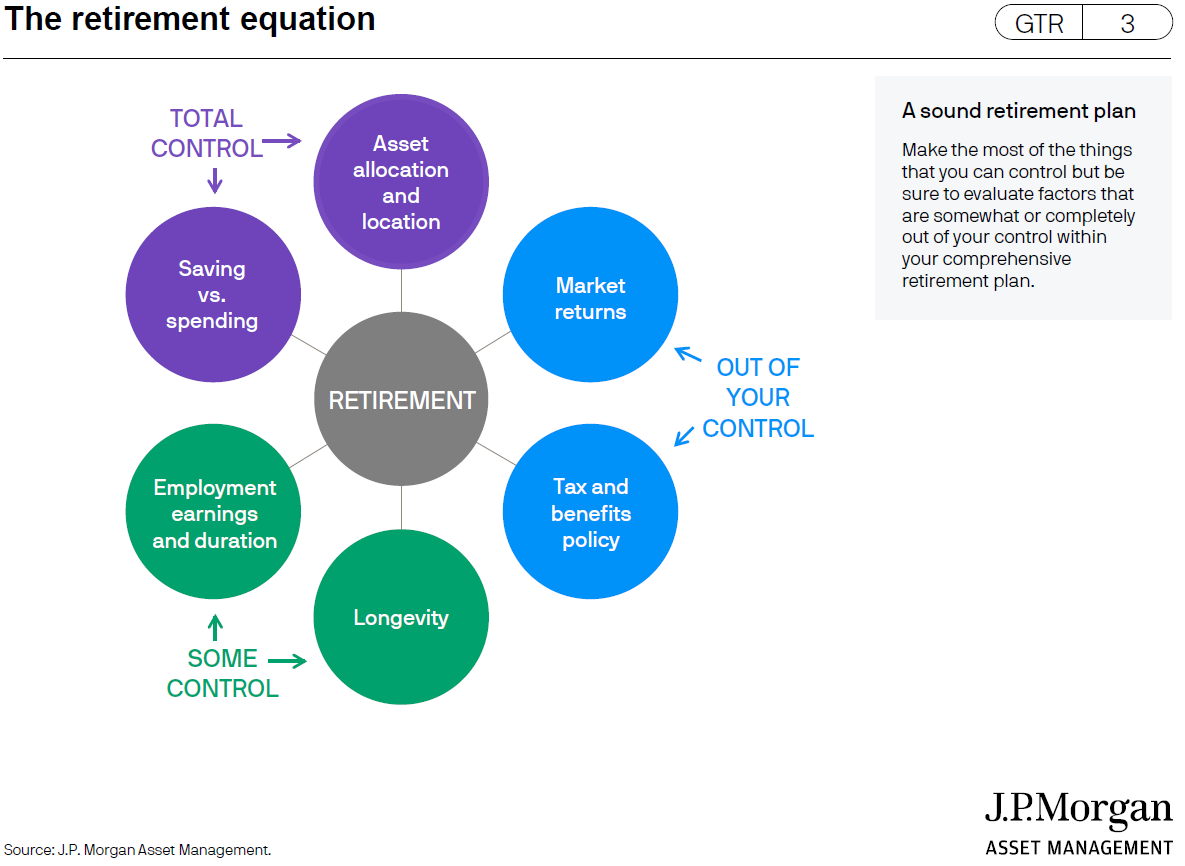

My control issues, of which there are many, serve as the lead-in to a discussion about how much control you get in relation to your retirement. In this newsletter, we’ll share some relevant charts from the recently released JP Morgan’s 2026 Guide to Retirement, so let’s start with a chart1 that visually depicts the numerous variables that relate to our own retirements.

Of the six essential components that comprise a sound retirement plan, we get to exert almost total control over two elements, have some control over two others, and have virtually no control over two other important components.

Out of your control:

Market returns: Let’s dispense with the argument that you, or virtually any other investor, can limit losses and maximize gains due to your innate ability to time the markets. While you can’t control how markets perform, you can control the percentage of your portfolio that gets invested in stocks and/or bonds, or in domestic equities vs foreign/emerging markets. But individual stock and bond market returns are what they are.

Tax and benefits policy: Unless you’re a US senator chairing the Ways and Means Committee, you have no control or input over this category. You may have some control over state taxes (e.g., you can move to a state that doesn’t tax retirement benefits), but we all have no control over Federal taxes.

Some control:

Employment earnings and duration: How long you work is dependent on a few factors, such as your health and the type of job you have. How much you earn while working is dependent on your skill set, education, and marketability. Given good health, you may have the ability to work a long time, though you may not always be employed in your career of choice. Get downsized while in your 50’s, for example, and age discrimination may limit your options going forward.

Longevity: We all have some input into our longevity. Exercise, diet, good dental care, and health screenings are within our control, while our DNA is not.

Total control:

Savings vs spending: Admittedly, lower-income earners have little say in how much they can save vs how much they spend. The reason is obvious: the first dollars out of all our paychecks go to shelter and food. If there’s nothing left after that, then there are no savings. If you move up the income scale, you get to make choices about lifestyle. Spend all of your discretionary income, and you’ve made the decision not to save. That would be your choice, not a decision dictated by others.

Asset allocation and location: These are bigger decisions than many people realize. While saving is important, the type of account in which funds are saved is also significant. If someone can effectively use ROTH IRAs, for example, they’ll have more after-tax dollars as they age. That means they’ll either have more to spend in retirement or have the luxury of not needing to save as much as once envisioned. After-tax dollars are generally the most desirable because no taxes are due when withdrawn from an account. Conversely, withdrawing funds from a rollover IRA is likely to result in both Federal and State taxes, thus reducing the net dollars to you.

If you’re a control freak like me, do the most with what you can effectively control. Save as much as you can, take care of your health, and try to add joy to your life. They may not allow us to fly the plane, but there’s certainly a lot we can do.

1 “The retirement equation,” Slide 3, Guide to Retirement, J.P. Morgan. 2026.

S.F. Ehrlich Associates, Inc. (“SFE”) is a registered investment advisory firm in New Jersey that offers investment advisory, financial planning, and consulting services to its clients, who generally include individuals, high net worth individuals, and their affiliated trusts and estates. Additional disclosures, including a description of our services, fees, and other helpful information, can be found in our Form ADV Part 2, which is available upon request or on the SEC's website at www.adviserinfo.sec.gov/firm/summary/121356.

If you are an existing client of SFE, it is your responsibility to immediately notify us if there is a change in your financial situation or investment objectives for the purpose of reviewing, evaluating or revising any of our previous recommendations and/or services.

This newsletter is for informational purposes only and is not intended to be and does not constitute specific financial, investment, tax, or legal advice. It does not consider the particular financial circumstances of any specific investor and should not be construed as a solicitation or offer to buy or sell any investment or related financial products. We urge you to consult with a qualified advisor before making financial, investment, tax, or legal decisions.

Information contained herein has been obtained from sources believed to be reliable. While we have no reason to doubt its accuracy, we make no representations or guarantees as to its accuracy. The opinions and analyses expressed herein constitute judgments as of the date of this newsletter and are subject to change at any time without notice. Any decisions you make based upon any information contained in this newsletter or otherwise are your sole responsibility.

No graph, chart, formula, or other device can, in and of itself, be used to determine which securities to buy or sell, or when to buy or sell such securities, or can assist persons in making those decisions.

Any securities mentioned in this newsletter are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell. There is no guarantee that a particular client's account will hold any or all of the securities mentioned in this newsletter. Additionally, from time to time, SFE’s officers, directors, employees, agents, affiliates, or client accounts may hold positions or other interests in the securities mentioned in this newsletter.

Any historical index performance provided herein is for illustrative purposes and includes the reinvestment of dividends and income, but does not reflect advisory fees, brokerage commissions, and other expenses associated with managing an actual client account. An index is an unmanaged group of stocks considered to be representative of different segments of the stock market in general. Index performance does not represent actual account performance. One cannot invest directly in an index. A description of each index mentioned in this newsletter is available upon request.

Any hypothetical performance shown or discussed herein is for illustrative purposes only. Hypothetical performance results have inherent limitations, including: they are generally prepared with the benefit of hindsight; do not involve financial risk or reflect actual trading; and do not reflect the economic and market factors, such as concentration, lack of liquidity or market disruptions, trading costs, and other conditions, that might have impacted our decision-making when managing actual client accounts. Since trades have not actually been executed, hypothetical performance results may have under- or overcompensated for the impact, if any, of certain market factors.

It should not be assumed that future performance of any specific investment, investment strategy, or index (including any discussed in this presentation) will be successful or profitable or protect against loss.

Any forward-looking statements or projections herein are based on assumptions. By their nature, forward-looking statements involve a number of risks, uncertainties, and assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. You should not place undue reliance on forward-looking statements, which reflect our judgment only as of the date this newsletter was published.