Fun With Charts!

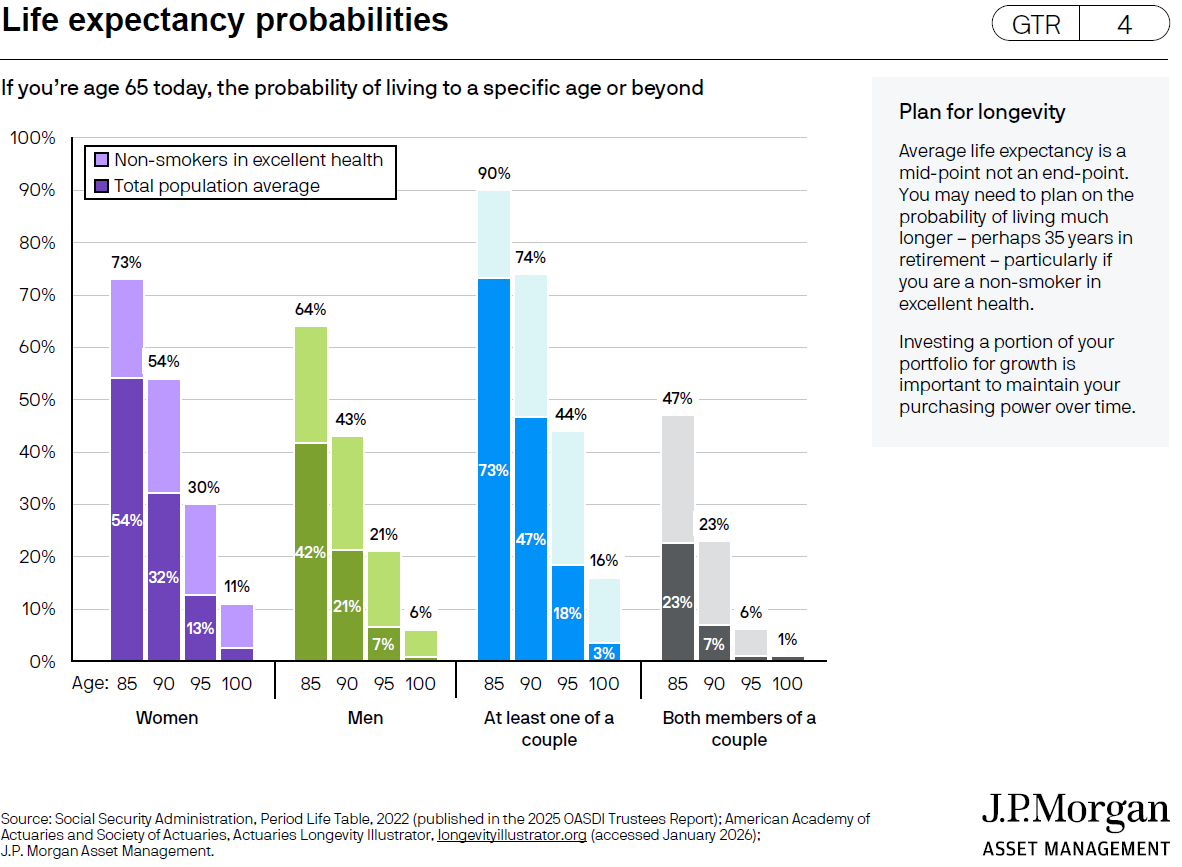

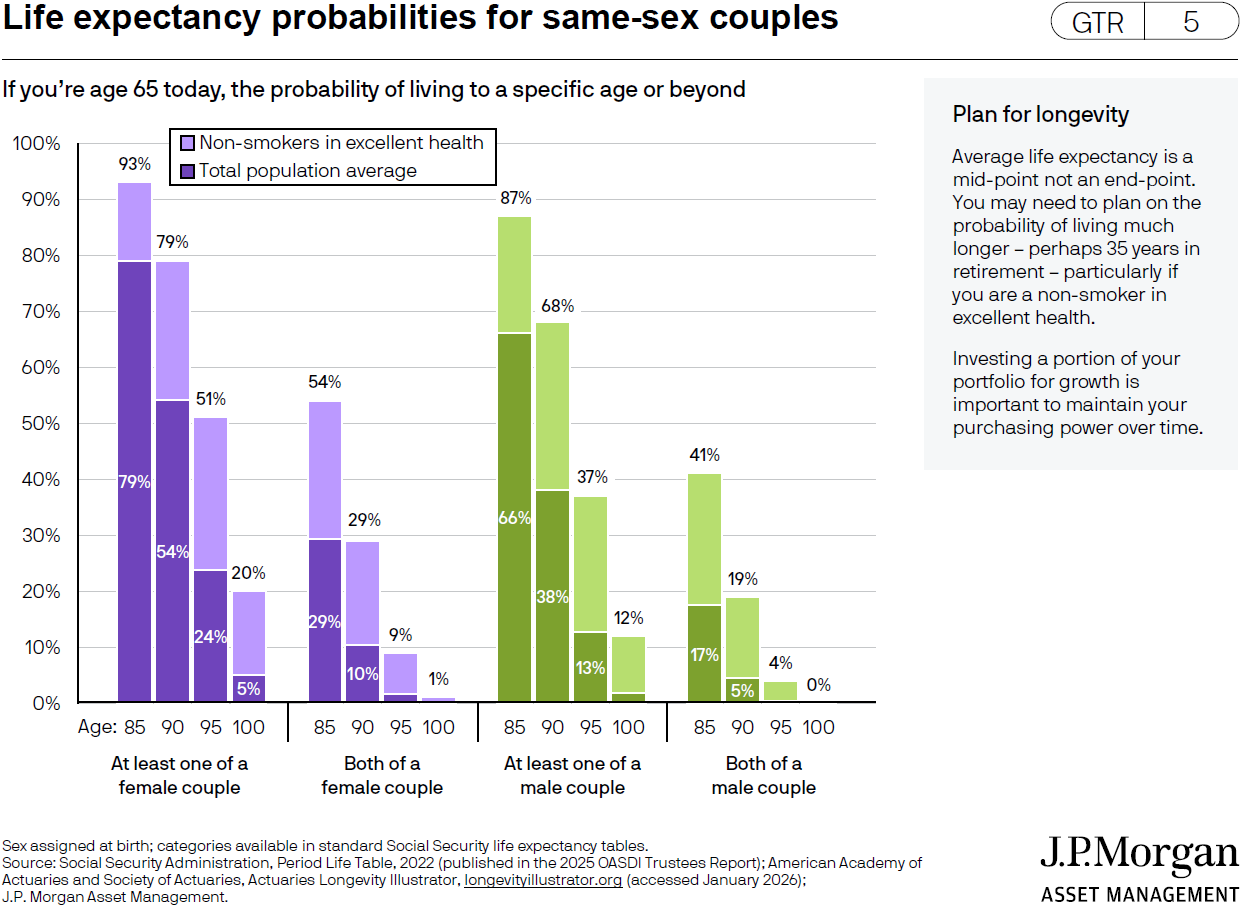

Life expectancy probabilities

While the good news is we’re all living longer, the bad news is we’re all living longer. Yes, it’s a bit of a dichotomy, but please read on to better understand how and why.

In the not-so-distant old days, retirees worked until age 62, got a handshake and the proverbial (or actual) gold watch, started collecting Social Security benefits, and didn’t count on an extended retirement. In contrast, the chart below1,2 shows that extended retirements are what a lot of us are likely to achieve.

For example, if you’re a 65-year-old non-smoking woman in excellent health, a surprising 11% of you will live to age 100. (100!) And if you’re a non-smoking 65-year-old man in excellent health, 6% of you will also live to age 100. Taken as a couple, 16% of non-smoking couples (aged 65) will have at least one member live to age 100. (So much for planning for 20-year retirements.) From an investment perspective, investing for the long-term is both necessary and required, with emphasis on the phrase ‘long-term.’

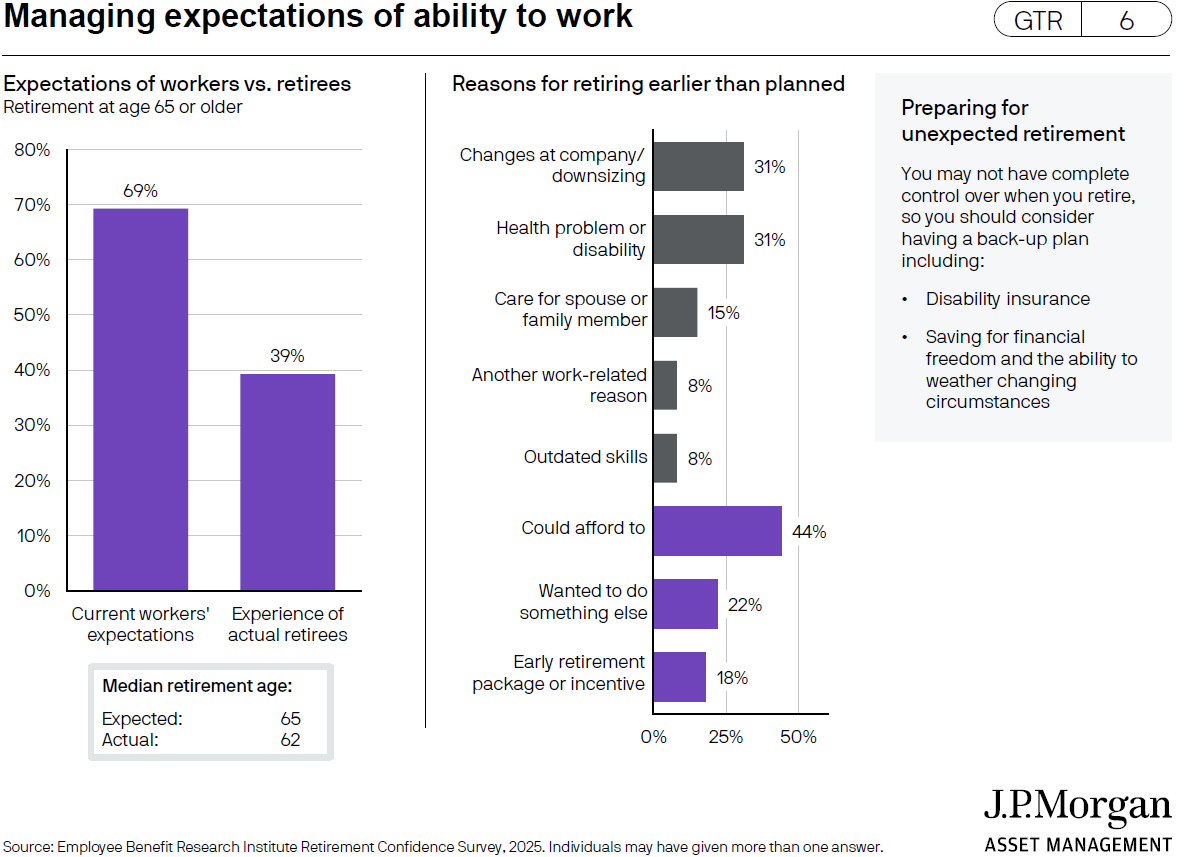

I’ll work at my job until they carry me out

Statistically speaking, that’s unlikely to happen. (They might carry you, but it would be part of a reorganization. And you’ll be alive, though probably a bit cranky.) 69% of workers expect to work until age 65, though only 39% do. And the chart3 below explains why it’s likely you’ll retire earlier than planned.

Work duration is a significant issue. If you plan on working for an additional X number of years and plan on saving Y amount of dollars each of those years, working less than X means it’s likely you’ll save less than Y. From a planning perspective, this is where contingencies enter the picture. You may, for example, have to work at a second (or third, or fourth) career. You may even have to work part-time instead of full-time.

Unfortunately, you may not know any of these things until you’re at, or near, the end of your career. And that helps to explain why financial planning is so fluid in nature; we don’t always know how the future will unfold until it unfolds. Retirement planning is all about contingency planning.

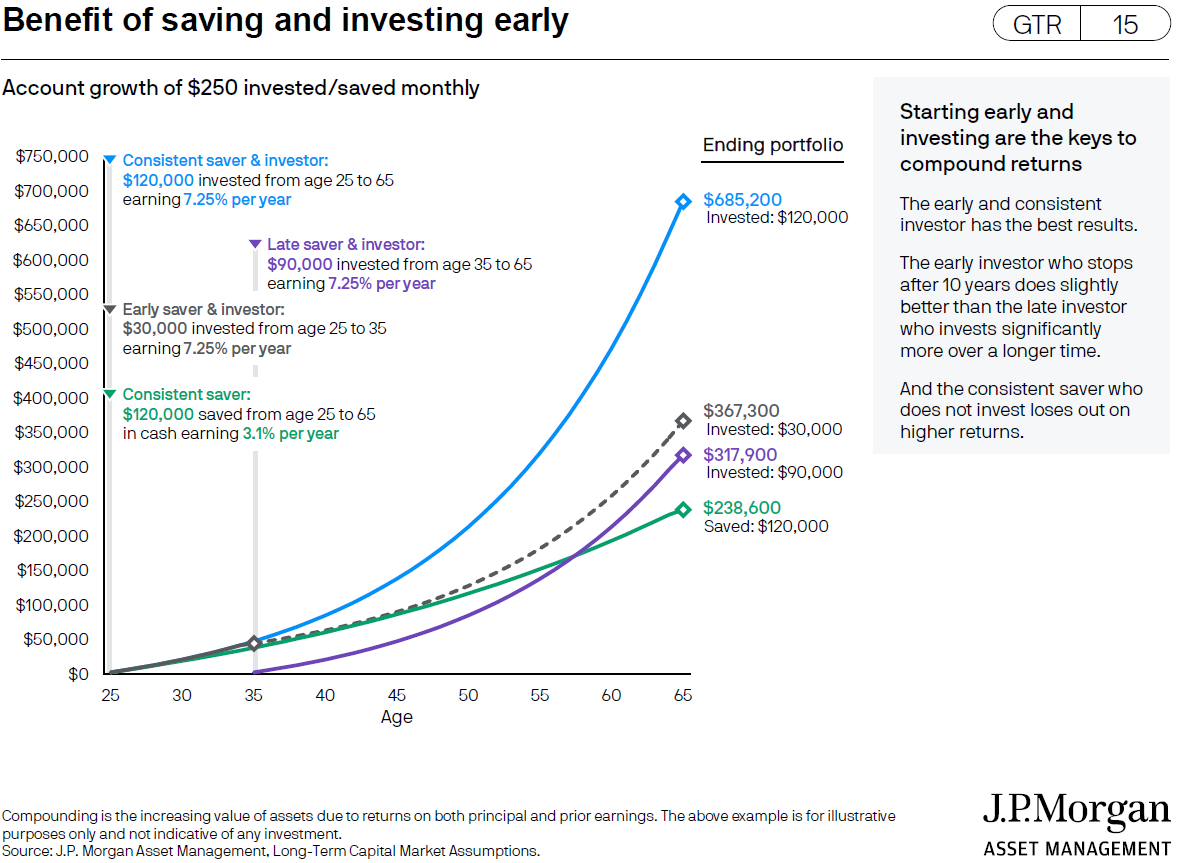

When it comes to saving, start early, and don’t stop

If you’re young and you’ve read this far, we tip our hats to you. It would be understandable if a twenty-something, or thirty-something (but not a forty-something!) read the words ‘retirement’ and ‘longevity’ and said: “Get me out of here.”

But if you stuck around, you’re probably one of those people who is a ‘consistent saver & investor,’ a person who understands the long-term benefits of investing early, and consistently.

As can be seen above4, ‘Consistent savers & investors’ who start saving (and investing) at age 25 and continue through age 65, have more assets than their counterparts who: (a) start saving later; (b) start saving early and then stop; (c) start saving early and consistently, but don’t invest their savings for the long haul. (An example of conservative saving vs investing is buying a CD vs investing in the stock market.)

Playing it safe may be a strategy, but it’s generally not the winning strategy for growing a pot of money that will last through retirement. Younger investors, especially, have the time to withstand the multiple ups and downs that come with investing. Much like the expression Ron Popeil used when selling Ronco Showtime Rotisseries on late-night TV in the 90s and early 2000s, “set it and forget it” is a good strategy for younger investors when it comes to retirement. (Just to clarify: instead of buying rotisseries, buy mutual funds and exchange-traded funds.)

1 “Life expectancy probabilities,” Slide 4, Guide to Retirement, J.P. Morgan. 2026.

2 “Life expectancy probabilities, same sex couples,” Slide 5, Guide to Retirement, J.P. Morgan. 2026.

3 “Managing expectations of ability to work,” Slide 6, Guide to Retirement, J.P. Morgan. 2026.

4 “Benefit of saving and investing early,” Slide 15, Guide to Retirement, J.P. Morgan. 2026.

S.F. Ehrlich Associates, Inc. (“SFE”) is a registered investment advisory firm in New Jersey that offers investment advisory, financial planning, and consulting services to its clients, who generally include individuals, high net worth individuals, and their affiliated trusts and estates. Additional disclosures, including a description of our services, fees, and other helpful information, can be found in our Form ADV Part 2, which is available upon request or on the SEC's website at www.adviserinfo.sec.gov/firm/summary/121356.

If you are an existing client of SFE, it is your responsibility to immediately notify us if there is a change in your financial situation or investment objectives for the purpose of reviewing, evaluating or revising any of our previous recommendations and/or services.

This newsletter is for informational purposes only and is not intended to be and does not constitute specific financial, investment, tax, or legal advice. It does not consider the particular financial circumstances of any specific investor and should not be construed as a solicitation or offer to buy or sell any investment or related financial products. We urge you to consult with a qualified advisor before making financial, investment, tax, or legal decisions.

Information contained herein has been obtained from sources believed to be reliable. While we have no reason to doubt its accuracy, we make no representations or guarantees as to its accuracy. The opinions and analyses expressed herein constitute judgments as of the date of this newsletter and are subject to change at any time without notice. Any decisions you make based upon any information contained in this newsletter or otherwise are your sole responsibility.

No graph, chart, formula, or other device can, in and of itself, be used to determine which securities to buy or sell, or when to buy or sell such securities, or can assist persons in making those decisions.

Any securities mentioned in this newsletter are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell. There is no guarantee that a particular client's account will hold any or all of the securities mentioned in this newsletter. Additionally, from time to time, SFE’s officers, directors, employees, agents, affiliates, or client accounts may hold positions or other interests in the securities mentioned in this newsletter.

Any historical index performance provided herein is for illustrative purposes and includes the reinvestment of dividends and income, but does not reflect advisory fees, brokerage commissions, and other expenses associated with managing an actual client account. An index is an unmanaged group of stocks considered to be representative of different segments of the stock market in general. Index performance does not represent actual account performance. One cannot invest directly in an index. A description of each index mentioned in this newsletter is available upon request.

Any hypothetical performance shown or discussed herein is for illustrative purposes only. Hypothetical performance results have inherent limitations, including: they are generally prepared with the benefit of hindsight; do not involve financial risk or reflect actual trading; and do not reflect the economic and market factors, such as concentration, lack of liquidity or market disruptions, trading costs, and other conditions, that might have impacted our decision-making when managing actual client accounts. Since trades have not actually been executed, hypothetical performance results may have under- or overcompensated for the impact, if any, of certain market factors.

It should not be assumed that future performance of any specific investment, investment strategy, or index (including any discussed in this presentation) will be successful or profitable or protect against loss.

Any forward-looking statements or projections herein are based on assumptions. By their nature, forward-looking statements involve a number of risks, uncertainties, and assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. You should not place undue reliance on forward-looking statements, which reflect our judgment only as of the date this newsletter was published.