Embracing a global stock market: why buy international stocks?

June 30, 2019

When the U.S. stock market goes up, it’s only logical to question why there’s a need to own anything but U.S. stocks. That argument can be further bolstered by pointing out how many U.S. companies derive sales from international markets. “If I own Coca-Cola, aren’t I invested internationally?”

A recent Vanguard paper1 highlights three major reasons to invest internationally:

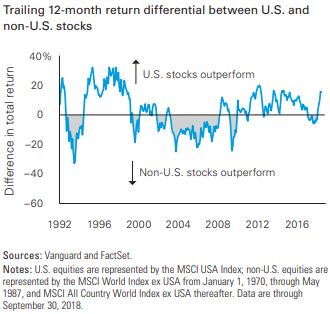

1. Changing market leadership: “The rationale for diversification is clear. U.S. and international stocks often swap positions as performance leaders…Global diversification gives you a chance to participate in whatever region is outperforming at a given time.”

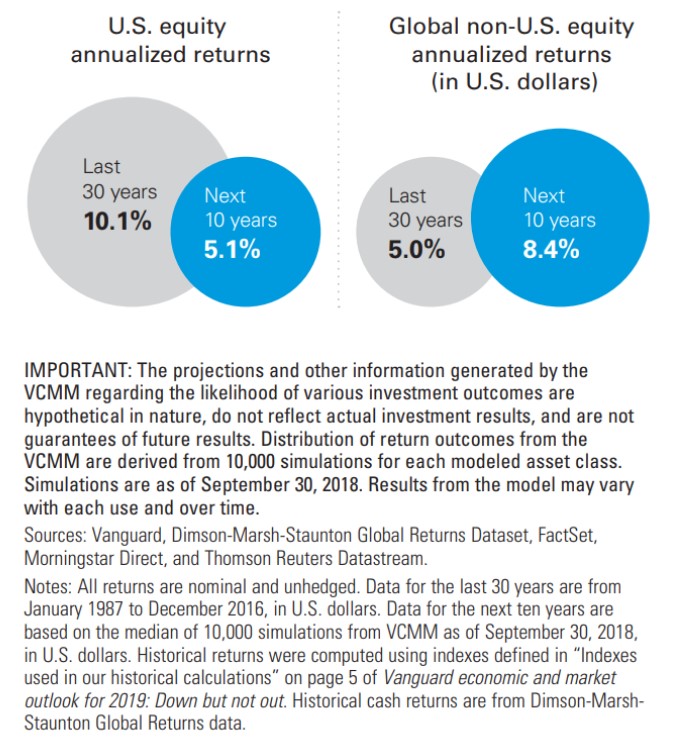

2. Positive international outlook: “U.S. stocks have had a great run, but will that continue? From a U.S. investor’s perspective, the expected return outlook for non-U.S. stock markets over the next 10 years is 8.4%, higher than that of U.S. stocks (5.1%).”

3. Volatility reduction: “Having a mix of international and U.S. stocks has historically tamped down the volatility in portfolios. Of course, it’s natural to be concerned about geopolitical risk, but having a mix of U.S. and international can actually reduce portfolio risk. It’s true that correlations have increased between U.S. and international markets as globalization has taken hold, but including international stocks in your portfolio still carries diversification benefits because of less-than-perfect correlations due to differences in economic cycles, fiscal and monetary policies, currencies, and sector weighting.”

As to why U.S. based companies with international sales can’t provide the same benefits as owning international stocks: “U.S.-headquartered multinational companies alone don’t provide enough exposure because a big chunk of the world economy is still driven by companies with headquarters outside the United States.”